Imagine you get your paycheck, you breathe a little, and make a quick plan in your head: “I’ll save ₦10,000, maybe even ₦20,000 to stretch things.” But by the time you’ve bought food, paid for airtime/data, and sorted transport for the week, all the money is mostly gone.

That’s the cycle many young Nigerians are stuck in.

Not because they don’t care about money, or aren’t trying to save. But because between low income, high costs, and daily pressure, there’s just not much left to work with.

In May 2025, we ran a nationwide survey with over 1,100 Nigerians aged 18–44 to understand how people save, spend, and manage money today. The findings point to a clear pattern: people want better financial habits, but survival often takes priority.

Let’s take a closer look at how that story unfolds.

The Reality of Spending in Nigeria Today

When we asked people what they spend money on each month, the answers were almost universal: food, data, transport, and helping family. Not travel or gadgets. Just the basics.

The numbers tell us even more:

- 72% listed food as a top expense

- 46% mentioned airtime and data

- 36% included transport

- 27% regularly support family

That doesn’t leave much wiggle room. And if you’re a student, a freelancer, or someone without a stable paycheck, that wiggle room gets even smaller.

Still, the desire to save is strong. More than half of respondents — 56.7% — say they save regularly, even if it’s a small amount. Another 22.2% save once in a while.

But the twist is that 1 in 5 people say they simply can’t save at all. Not because they lack discipline, but because they don’t earn enough. Or what they earn barely covers the week.

So the money comes in, and in a few days, it’s already gone. They’re not careless, costs are just getting too high lately.

Nigerians Are Budgeting, But The Budget Often Breaks

Even in the middle of all this pressure, people are trying to plan. They’re not giving up. In fact, many are doing what any personal finance guide would recommend.

- 69% of Nigerians in the survey said they set a savings target every month.

- 68% keep a personal budget or expense plan.

That’s not a sign of financial laziness, but of commitment. People know what they should be doing. They’re making the effort.

But then, life happens.

Prices go up. An unplanned bill shows up. A family member needs help. Or maybe there’s a tempting sale and it feels like a now-or-never deal.

That’s where the budget cracks.

Only 35.3% of respondents said they reached a savings goal in the last month. And 17.1% admitted they often overspend, even with a budget in place.

The reasons? Mostly beyond their control:

- 45.6% said they overspent because they underestimated how much things would cost

- 28.8% pointed to emergencies

- Just 16.8% said they knowingly ignored their budget

In other words, overspending isn’t a discipline issue. It’s a planning mismatch, caused by fast-moving prices, unpredictable needs, and not enough margin for error.

And when things go off track, emotions kick in.

41.6% of respondents said they felt regret after overspending.

Another 38.4% felt motivated to try again. That’s a powerful signal: people want to do better. They just need the right support to keep trying.

What’s Missing From Nigeria’s Fintech Solutions

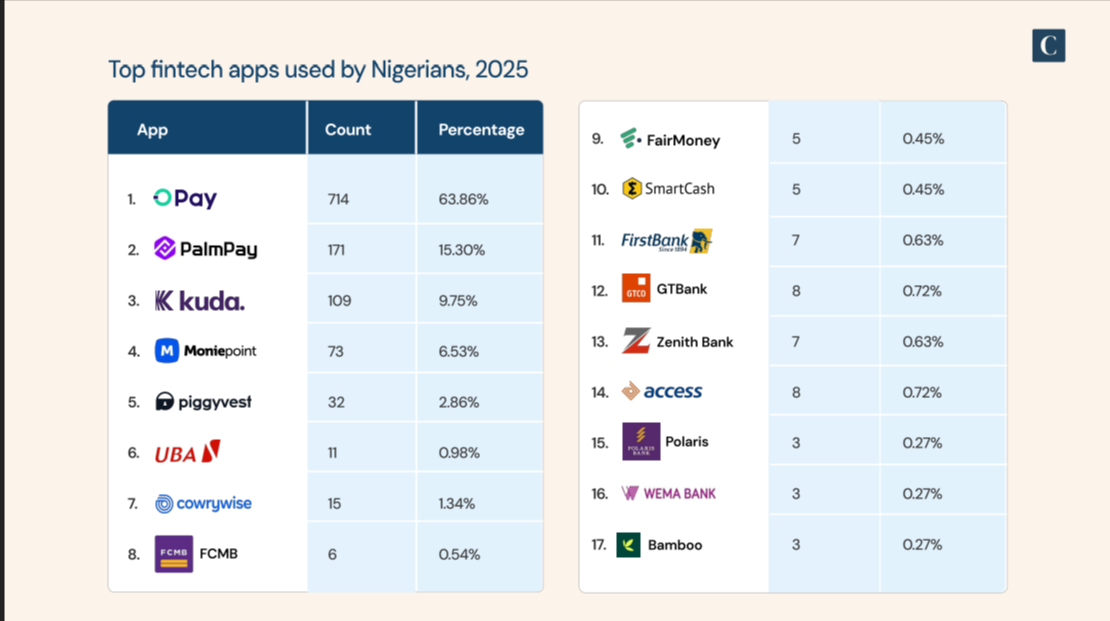

Most people already use financial apps. Not just one, but several. In fact, nearly 9 in 10 respondents said they use between one and three apps to manage money. And platforms like Opay are leading the way, with 63.9% of users naming it as their go-to.

So clearly, access isn’t the problem. Awareness isn’t either. People are already living digital-first financial lives.

The problem is, many of these tools aren’t built for the actual conditions people face — tight budgets, unpredictable income, and decision fatigue.

For example, when we asked what users want most from a money app, the answers were sharp and consistent:

- 65.7% want automatic savings

- 75.2% want a single place to see all their financial activity

- Others pointed to things like locked savings, spending reminders, and budget planning

These aren’t fancy requests. They’re just practical ones.

But in reality, most people are still tracking expenses manually — in notebooks, notes apps, or just their memory.

Only a small percentage use tools that show them how much they’ve spent, what they have left, or where their money’s actually going.

Why?

A lot of apps are built for what users should be doing — not what they can do today.

They expect stability. Predictability. Routine. But most users are dealing with the opposite.

When prices shift from week to week and your income is inconsistent, strict budgeting starts to feel like guesswork. And eventually, people stop trying.

The right tool, then, isn’t the one with the most features. It’s the one that adapts to this reality — offering simple, automated, low-effort support. Tools that nudge people forward without making them feel like they’ve failed when life happens.

How Nigerian Banks and Fintechs Can Better Support Users

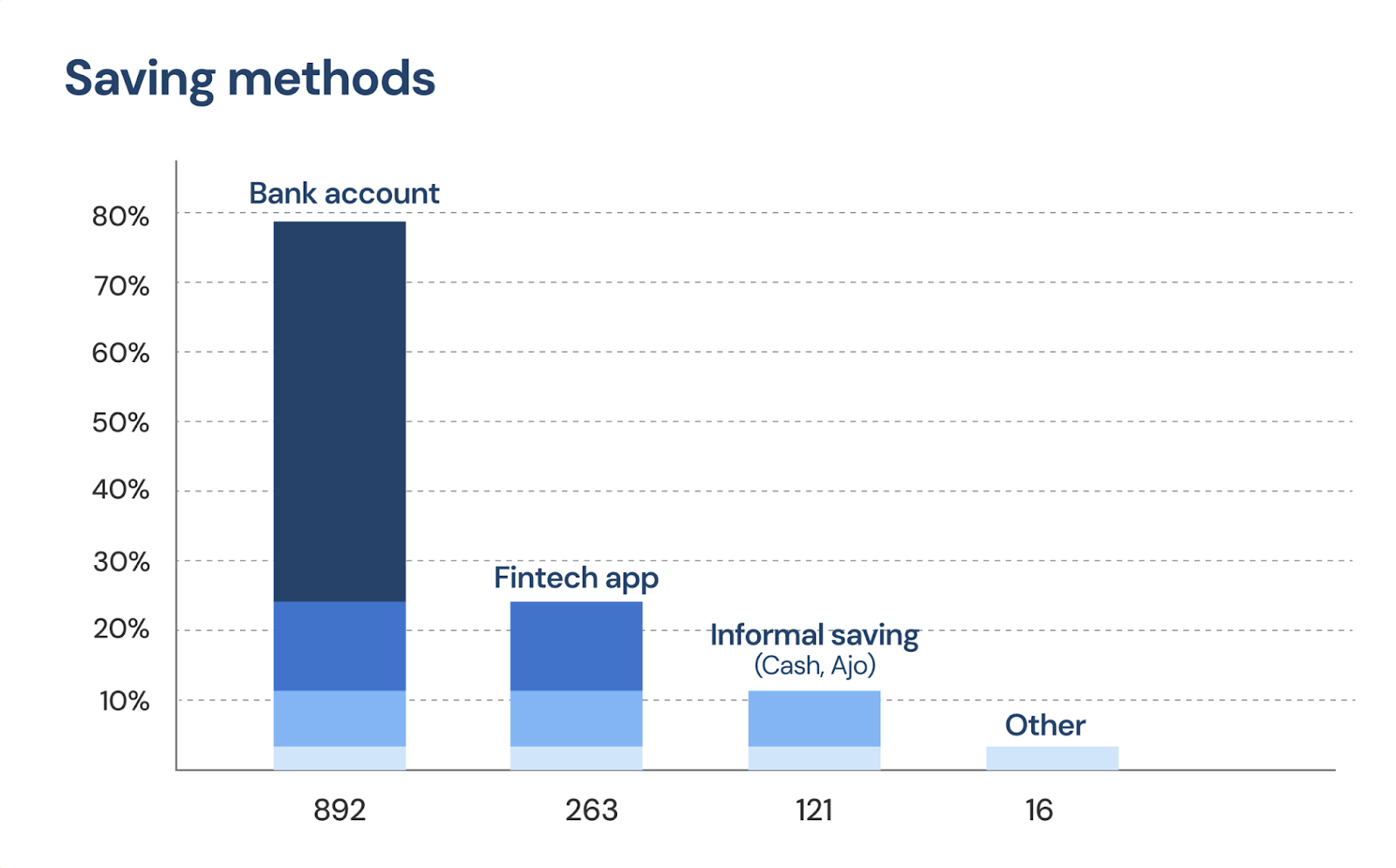

Local banks are still the most trusted place to store money. 79.3% of survey respondents said they save in a traditional bank account. That’s a big number — and it shows that banks still hold a strong position in the financial lives of Nigerians.

But storing money isn’t the same as managing it.

Most banks today act more like vaults than partners. Their apps let you check your balance and send money, but they rarely help you build habits, stay on budget, or reach a goal.

That’s a problem. Users aren’t just looking for storage anymore.

They’re looking for structure.

Meanwhile, fintechs are making moves. Apps like Opay, Palmpay, and Kuda have earned user trust with speed, flexibility, and ease of use. They’re part of daily life. But even then, they’re mostly being used for day-to-day transactions, not deep financial planning.

There’s a disconnect here. People are using the tools, but not in a way that builds lasting change.

And yet, the demand is crystal clear. Nigerian users are asking for:

- One place to track all accounts

- Automatic savings tied to behavior

- Budget tools that actually work in real life

- Reminders and nudges that feel like guidance, not guilt

To deliver on this, both banks and fintechs need to rethink their roles. They need to shift from offering products to building partnerships that work quietly in the background to help users stay on track, even when life gets unpredictable.

One step in that direction? Open banking.

It’s already been introduced in Nigeria, but uptake is still slow. And yet 75.2% of respondents said they want to see all their financial activity in one place. That’s a strong signal, and an open invitation.

The tools are here. The users are ready. Now it’s time for financial providers to meet them halfway.

The Bigger Barriers to Financial Stability in Nigeria

No matter how smart or user-friendly an app is, it can only do so much in isolation. Because underneath the day-to-day money struggles lies something bigger: a system that isn’t built for people who live on the edge of enough.

In our survey, 19% of respondents said they can’t save at all. Not because they don’t want to, but because their income is too low, too unstable, or both. Many are students, freelancers, or self-employed workers whose paychecks come irregularly — if at all.

That makes planning nearly impossible. Add rising prices to the mix, and budgeting starts to feel like a moving target.

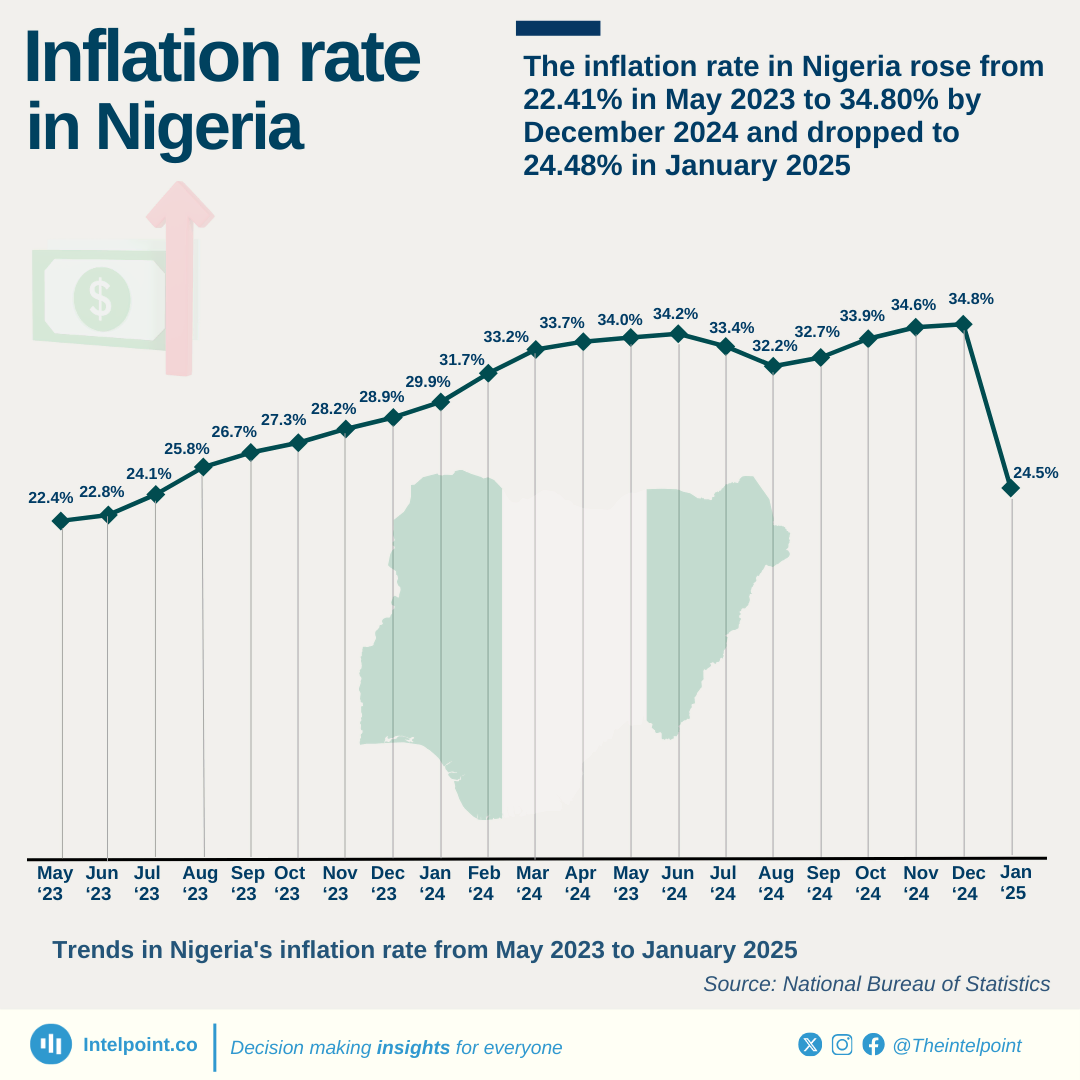

In 2024, Nigeria’s inflation hovered above 30% for most of the year. Even after easing to around 24% in early 2025, prices remain volatile. One week, transport costs this. The next, it costs that. And that unpredictability chips away at even the best-laid financial plans.

It’s no surprise that 36.9% of respondents said they don’t track their expenses at all. When money moves fast and nothing stays steady, tracking feels like a luxury — something for people with more time, margin, and certainty.

So what can be done?

This is where the Nigerian government has a key role to play. Not in replacing innovation, but in setting the stage for it.

Here’s how:

- Support steady income streams for young people — through jobs, grants, or small business support

- Promote financial literacy that’s practical, local, and built for mobile

- Lower data costs by helping telcos expand access and reduce overhead

- Accelerate open banking adoption so people can finally get a full picture of their finances, all in one place

- Update digital finance policies to match how people actually use these tools — not just how systems expect them to

When public infrastructure improves, private tools work better. And when both come together, users finally have a real shot — not just at saving, but at staying saved.

What Telcos and Retailers Can Do for Financial Wellness in Nigeria

We often think of saving and spending as personal choices. But in reality, they’re shaped by what’s happening around us — by how products are priced, how data is sold, and how businesses encourage (or discourage) smarter habits.

Let’s take telcos, for example.

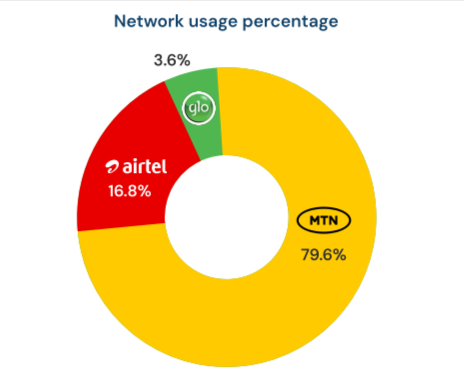

Airtime and data are the second most common expense after food — mentioned by 46.1% of respondents. And one provider, MTN, dominates the space, with nearly 80% of users on its network.

That kind of reach isn’t just commercial power. It’s an opportunity.

What if telcos offered reward bundles tied to saving milestones?

Or discounted data for users who hit their monthly financial goals?

What if mobile providers weren’t just selling connectivity — but helping people stay on top of their money?

In the same way, retailers have influence too. Whether you’re selling groceries, transport cards, or airtime vouchers, you’re part of someone’s monthly rhythm. And that means you can support better habits.

Here’s how:

- Bundle everyday essentials at a small discount to help users stretch their budget

- Let customers save toward a product over time (“Save ₦500 weekly for this item”)

- Build budgeting or expense summaries into your app so people can see what they’ve spent — and what’s left

It doesn’t have to be complicated. Even a small prompt — “You’ve spent ₦3,000 on snacks this week” — can spark better decisions.

And if you’re running a promotion? Remember: 40.6% of impulse spending is triggered by discounts. That means your offer has power, but also responsibility. Push too hard, and users feel manipulated. Use it wisely, and you help them buy better, not just buy more.

Retailers and telcos don’t have to become financial institutions. But they can become financial allies , just by understanding where their products fit into people’s lives.

Our Findings Made Waves in the Media

Since the survey report was published, several media outlets have picked up the story — digging into what the data reveals about how young Nigerians really manage money.

Here’s where the conversation has continued:

- TechBuild Africa explored how digital tools are falling short despite widespread use

- Nairametrics highlighted the disconnect between fintech features and real behavior

- The Nation covered the growing trust in fintech platforms for saving

- This Day focused on the broader pressures facing Nigerian youth

The media response confirms what the data already suggested: these aren’t isolated experiences. They’re shared struggles — and the solutions need to be just as widespread.

The Saving Struggle in Nigeria Is Bigger Than Personal Effort

Young Nigerians are doing their part. They’re budgeting, setting goals, and using apps. But the system around them — rising costs, unstable income, disconnected tools — makes it hard to follow through.

The intent is there. The effort is real.

Now, it’s on banks, fintechs, policymakers, and brands to meet people where they are. To build tools that are simple, supportive, and fit real life, not just ideal conditions.

Saving shouldn’t be a luxury. It should be something the system helps you do — even when money is tight.

This article is based on findings from Column’s Nigeria Financial Habits Survey 2025. Read the full report here for more insights.